It might be hard to fathom now, but someday, you will exit your business. The decisions you make now will determine if it’s on your terms or not. If you are one of the savvy few, you will prepare today for the eventual sale of your business. This includes avoiding mistakes that will hurt your business sale in the future. For most, this is the ideal outcome. Upon success, you could have the financial freedom to do what makes you most happy. After all, you started your business to build an asset.

Here are 5 common mistakes that will hurt the sale of your business.

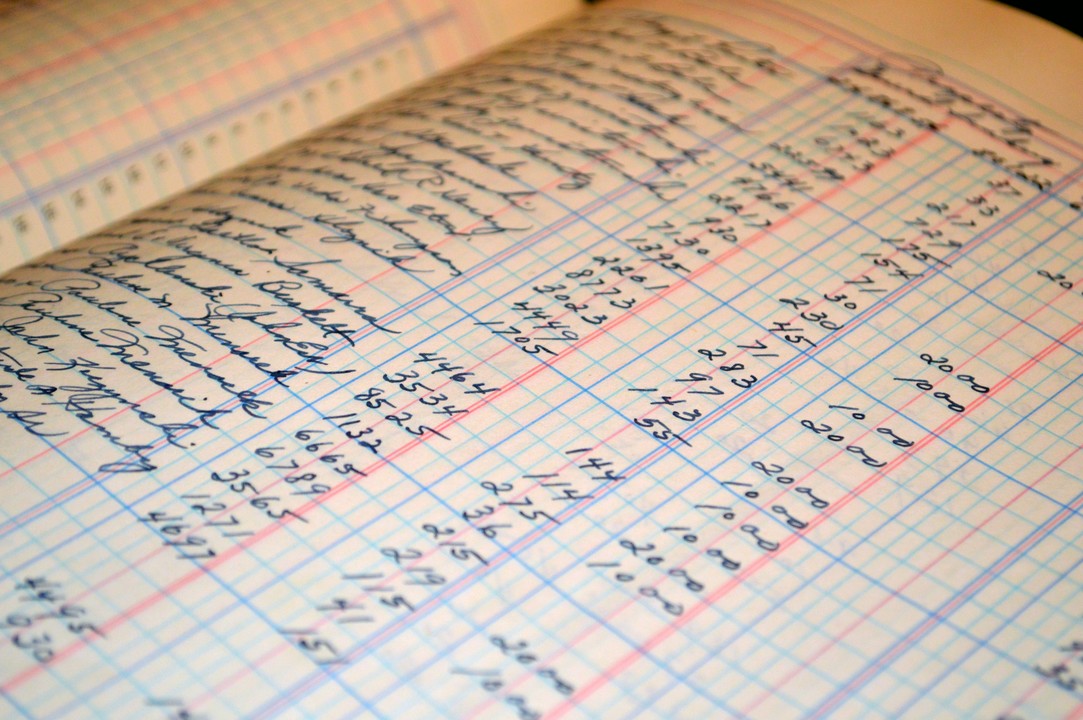

Poor bookkeeping

It may be tempting to keep your financial records the old-fashioned way through a handwritten ledger or Excel files. Resist that urge. It is absolutely a necessity that your bookkeeping is done through a widely recognized accounting software like Quickbooks. Buyers need to see solid record keeping. It tells a story about your business. Pouring through a pile of notebooks do not give interested parties peace of mind.

The more data the better. It allows you to pinpoint specific periods of time and make better decisions. Large amounts of information that are easily accessible reduce risk and give buyers the confidence they need.

If you need another reason to keep electronic books, it’s because the money you save on software you will give back to your accountant in hourly fees and it will likely cost you more. Making sense of chicken scratch is expensive.. if you can find an accountant willing to work with you.

Be familiar with your numbers and be able to answer simple questions about your financial health. You should know details including:

- how much money is owed to you

- how much you sold last month

- what outstanding bills you have

If you can’t answer these questions within reasonable ranges off the top of your head, you are not paying close enough attention.

Trading volume for margin

Buyers tend to focus on Earnings Before Taxes, Interest, Depreciation, and Amortization (EBTIDA). This means regardless of volume, you must also concern yourself with margin. This is loosely defined as the difference between what it costs to produce your product or service versus what you actually sell it for after all expenses are paid.

Transworld Business Advisor, Bianca Evans sees this frequently. She explains “This phenomenon happens quite often especially with established businesses. The business owner feels indebted to longtime customers that have been with them since nearly the beginning. The business owner is hesitant to raise prices to keep pace with inflation or rising product costs because they don’t want to damage any relationship they have built over the years. Somewhere along the way, it becomes more personal than business.”

That’s understandable because every business is built on solid relationships. But, it could be time to look hard at these numbers. Fixing them could mean a drop in overall sales. But, profit could remain similar or even increase.

Not paying for experts

Getting the big three in your corner is going to be important for the entire life of your business. Solid relationships with an attorney, banker, and certified public accountant will pay dividends. Yes, they are expensive. But not nearly as costly if you make just one wrong decision without consulting with them. Make sure they understand your business model well and check in with them frequently. Setting quarterly lunch dates is a good idea.

Face your demons

“Nothing kills a deal faster than surprises” warns Evans. When buyers do their due diligence on your business they will find all the skeletons. It’s best to reveal them early in the process so they don’t become larger issues later. Better yet, deal with those nagging issues before you decide to sell your business. Examples could be, outdated lease agreements, liens on your property, cases of existing or pending lawsuits, or any other issue that would give a buyer pause. Don’t try to hide these things. Because when discovered, the buyer will wonder what other issues have been non-disclosed.

Over-leveraged with one client

Be careful of having too much business with anyone or a small group of clients. On the surface, your business may appear to be healthy. But just one unforeseen event could put you out of business. Buyers will likely stay away if they see you are overleveraged. Or it could have a significant negative impact on the price you get for your business.

Evans recalls one real-world scenario of a repair business that was doing well. But most of the business came from one commercial account. When questioned about it, the business owner dismissed the conversation. The business owner stated that they had a solid relationship and they were personal friends. Shortly after, the devastating call came. A larger organization had purchased the customer. The fleet maintenance was going to be outsourced to someone else through a national agreement. Overnight business dropped 40% and it was devastating. Ultimately it was too much to overcome and the business closed its doors.

So there you have it. 5 mistakes that will rob your business of its value. Avoid the missteps of others and chart your own path to success!